Game Development Trends in 2024: Crisis and Opportunity

At the start of 2024, there’s a shift in both the types of games people want to play—as well as the way these games are made. At times, it feels like a crisis. But it is also an opportunity for those who invest wisely.

This is a long article, so here’s what I’m going to cover:

Revenue Down, Costs Up (i.e., why layoffs are happening — and what must be done about it)

“This Game is Fun, Bro” — the divide between the mainstream gaming markets and what vocal groups claim on social media; the importance of a great game.

What spatial computing will and won’t do for gaming

The disruptive effect of creator-led platforms

Longer-term impact of Apple’s adversity towards developers

The Web Renaissance—what’s going to happen due to WebGPU, and the relative disadvantage of native mobile marketing, and other technological innovations

Cracks in the 3D Engine market—developer willingness to switch engines

Next-gen rendering pipelines (Unreal 5 innovations, Gaussian Splats, etc.) and what they mean

The strength of PC Gaming

The growth of UGC within PC games

The importance of IP, and how it’s shifting towards game-first IP

Impact of Generative AI on both production and in-game experience

Importance of decentralized AI

The state of open-economy (blockchain and other) games

Phew—that’s a lot! But nobody said leading game projects in 2024 was going to be easy. Let’s begin:

Revenue Down, Costs Up

When you look around the gaming landscape, it seems like an industry in crisis: hardly a day passes without word of a new layoff.

The reasons aren’t complicated: after a short-term, lockdown-induced surge in revenue, 2023 industry revenues were down in real-dollars, while labor costs are higher than ever. Although the industry is going to continue growing from here—it’s the media category of the 21st century—a reset was somewhat in order:

And while I can only feel heartbroken for game developers who recently took jobs, relocated and got new mortgages (something that might have been mitigated by leaning into remote work)—it’s hard to criticize game executives for reallocating capital in the face the economic realities, or for rolling the dice on new ideas 4 years ago in the midst of a ZIRP-fueled capital boom (and providing work at a time when things looked bleak).

“This Game is Fun, Bro”

There’s simply no replacement for a fun game. This player of Palworld sums up what the mass-market actually cares about—and it isn’t philosophical stands on generative AI, the inside-baseball travails of crunch or labor conditions, or whether a game uses a particular 3D engine or server technology. That’s not to say that these things aren’t interesting or important debates within the world of game development, but one must be certain to operate in the world one actually is in, not the one you think we ought to be.1

With 14,000 games released on Steam last year and millions of apps on mobile, it’s critical to remember that“this game is fun, bro” is what you need your audience to feel. The magic of game development is finding an audience that you can convey that feeling to, and building the game they most desire.

I love AAA games as much as anyone: Baldur’s Gate 3 was my favorite game last year, and one of my favorite of all time. The craftsmanship of these games is amazing. But Palworld illustrates how a small team (estimated at 10-20 people) can create a hit game. It also shows that technological trends including modern 3D engines, live services platforms, generative AI, asset stores, and UGC are not only democratizing development—but increasing the ceiling on what a small team can accomplish.

In today’s market, it is more important than ever to:

Understand your audience

Build them the game they love

Find more of the players who are right for you

Sustain their engagement

Increase development velocity

Decrease development & live ops risks

Palworld is part of the small-team approach to game development I’ve commented on several times over the last few years. Other games made by small teams include Hollow Knight, Valheim, Stardew Valley and Undertale. It also includes the new breed of games being made in platforms like Roblox.

Spatial Computing Won’t (Soon) Disrupt Games

Follow up article: Spatial Computing Won’t Disrupt Games - Games Will Disrupt Almost Everything Else

Although the launch of the Vision Pro in 2024 is a significant moment in the maturity of spatial computing, games with Virtual Reality (VR) and Mixed Reality (MR) are not going to be disruptive to the industry. That said, we’ll continue to see very interesting and innovative products that appeal to headset owners.

For something to be “disruptive,” it means expanding the size of a market by making a previously-scarce product or service available to a much larger audience, typically by a business model that dramatically lowers cost or a technological transformation that makes the market far more accessible, replacing incumbents in the process. The last truly disruptive technology in video games was free-to-play mobile, which added billions of players. Today, half the industry’s revenue is generated by mobile.

With more than 3 billion players in the world, AR/VR might find some people who simply wouldn’t play a game any other way—but most likely, this will be a modest increase in total market size. That’s not to say that there won’t be lots of innovative products that shift spending away from other platforms—or that there won’t be lots of great game ideas that do something completely novel. Games like Beat Saber, Demeo and Cubism are a handful of examples of what wouldn’t or couldn’t exist without spatial computing.

Spatial computing will probably be disruptive to a whole range of other industries: education, fitness, travel—to name a few. These are industries that remain inaccessible to a huge part of the world, and desperately need technological solutions.

The main constraint for games is that there are not yet enough devices in the world (the market leader, Meta Quest 2, has around 20 million units) and that limits how many software units can be sold. Sales on the Quest series of headsets is comparable to software sales on the Wii-U (a canceled platform):

Spatial computing platforms are growing at a slower rate than smartphones did from the launch of the iPhone; the latter had sold 160M units from launch, compared to the 20M or so Meta Quest units. That said, it’s fair to say that mobile phones were already a well-established market when Apple introduced the iPhone, and spatial computing is still getting started.

The Vision Pro sold around 200K at debut, which isn’t a huge number, and isn’t a surprise given the price-point. It’s also noteworthy that Apple is still developing the market and this is really a dev kit, and the killer app is still to-be-determined (maybe it’ll be re-experiencing memories,” as some have pointed to).

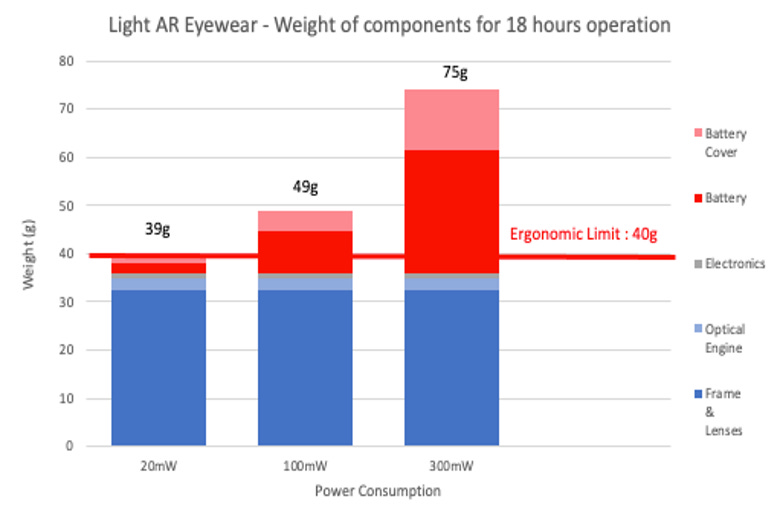

When will spatial computing get really huge? It’ll be a function of ergonomics. The ultimate form-factor would be a sunglasses-sized device that works all day. That will require further advancements in materials, computation, AI, and especially batteries. Studies have shown that the ideal weight is about the same as sunglasses—substantially less than either the Meta Quest 3 or the Vision Pro:

It will likely take a number of years before we see devices that reach these specs. Meta’s first real smartglasses are targeted for 2027. Once they do, it’s possible smartglasses will disrupt smartphones, unlock a new range of applications that wouldn’t be feasible without all-day, pervasive use. When they do, games may finally find a mass-market to pursue.

Until then, it’ll be the domain of a few developers who would be advised to keep teams lean so that they have the runway and agility to build beloved (and lucrative) products that connect with the spatial computing audience.

If you liked this section, please read the follow-up article: Spatial Computing Won’t Disrupt Games - Games Will Disrupt Almost Everything Else

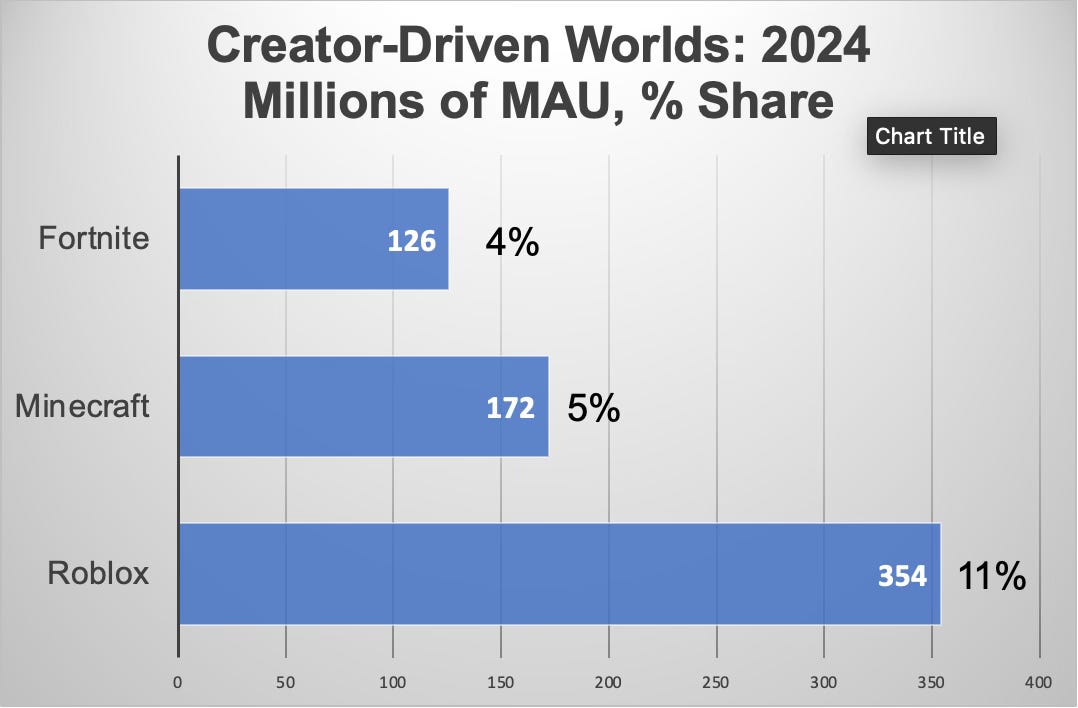

Creator-Driven Worlds Disrupt Traditional Gaming

The three largest creator-driven worlds are disrupting game development, in that they’re democratizing the ability to create games amongst people who previously would have lacked the skills or wherewithal to do so.

The usual counterargument is that these platforms target children who are less sensitive to the production values of modern games, but this is mistaken on two fronts. Let’s look at some realities from the largest of these platforms, Roblox:

Last year, the fastest-growing age group on Roblox was 17-24 year olds.

Production values of Roblox are improving substantially. And although they don’t currently come close to AAA quality, you’ll see that there’s a lot more possible than you might have expected:

Cracks in the 3D Engine Market

Currently, 66% of professional game development uses Unity or Unreal. But this market hasn’t really consolidated, and many developers are open to a switch:

Anecdotally, I’ve observed that most people currently considering a change are looking to move from Unity to some other engine (usually Unreal) rather than the other way around. Based on other data in the survey, it does illustrate that there are a number of opportunities in the market:

It’s Unreal’s market to lose—most developers leaving Unity will consider UE5 before looking at anything else.

Currently, only 5% of professional developers are targeting creator-driven (the so-called UGC platforms) like Roblox. The willingness to revisit choices like engine, along with a willingness to revisit everything—is an opportunity for the UGC platforms to absorb talent (especially with recent layoffs) that historically went with traditional engines.

It is also an opportunity for up-and-coming engines like Godot, Babylon, and Flax to prove themselves.

Unity is strongest on mobile, which is where Unreal is less focused (and has outright animosity). Maybe this is another opportunity for the emerging 3D engines as well.

Apple’s Adversity with Developers

History is replete with the downfall of platforms that became adversarial with too many of their own developers; and that appears to be the current situation with Apple.

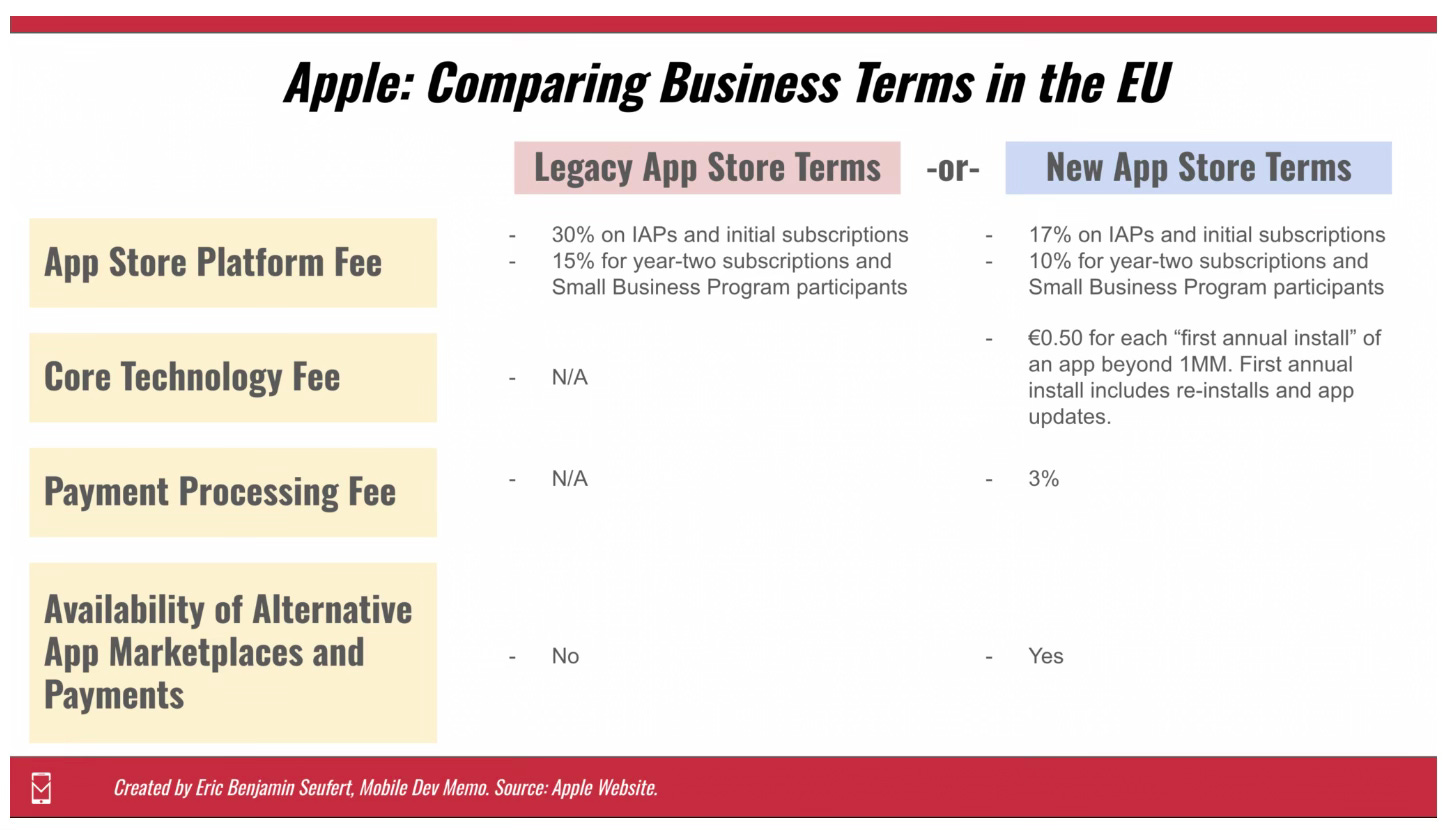

When the App Store was originally launched in 2008, developers celebrated the opportunity to ship products in a relatively non-competitive ecosystem, supported by featuring that could rapidly launch products into popular culture; and the 30% cut seemed reasonable relative to the high cost of traditional software distribution (65%+ on store shelves) or previous mobile platforms (often 50%).

Over time, the App Store swelled to millions of apps, and the the value of product featuring diminished substantially. Today, most of the benefit of the App Store is the low-friction of its payment ecosystem. At the same time, Apple has actually made it harder to connect with consumers, by making performance marketing more expensive and less effective since the release of App Tracking Transparency. Over time, they’ve hesitantly added-back some features of ad networks, such as conversion optimization—and while SKAdNetwork 5.0 promises to reintroduce re-engagement tracking—overall, the software distribution network ecosystem has become more of a tax than a value to developers.

Where Apple has prevailed in the courtroom (such as in the Epic lawsuit), they’ve lost somewhat to regulators. And in those cases, their compliance could be deemed to be passive-aggressive. In the face of regulators demanding that Apple permit third-party app stores, consider how Apple has responded by eviscerating their economics by introducing run-time fees, conversion-reducing “warning screens” and commissions that disgorge any potential upside:

Will any of this change in 2024? Perhaps not—there’s still plenty of good economic reasons for developers to release a game on iOS—particularly for cross-play titles where the revenue can be regarded as incremental. And regulators, while annoyed by Apple’s “compliance” might not act quickly.

Nevertheless, Apple’s moves are likely to push developers leaning towards other platforms. If developers derive greater profits on other platforms, it’ll produce a natural flywheel where more of the R&D goes elsewhere. Consumers love Apple products2, and are likely to keep buying them. But it can’t be good for the long-term health if Apple becomes a distribution platform for “incremental revenue” rather than core innovation. I’ve watched this movie a few times before, and when a platform becomes this adversarial to developers, it doesn’t end well. You can see that happening now with the Unity’s introduction of runtime fees.

And speaking of movies, the absence of Netflix as a launch app on Vision Pro is very telling.

The Web Renaissance

But where else are developers to go? One category I’m excited about is Web-based gaming. This is driven by a combination of technical and business innovations:

The largest constraint for games on the Web has been the large gap between graphical performance relative to what a native app can generate. However, WebGPU, which lets you program more directly to graphics hardware, has recently reached maturity and early demos show that it can deliver 60 fps performance for 3D graphics that were previously only 20-ish fps on WebGL.

The marketing ecosystem for the Web is mature and lacks the centralized control of a party such as Apple, who can undermine business plans for an app any time they want. However, there’s a lack of a large distribution hub for Web based games and most developers in there post-social-games era have forgotten how to do effective performance marketing (one to keep an eye on is FRVR).

Web-based financial rails are worse than the relatively frictionless environment of iOS, Android, Steam, etc.—although platforms like Shopify and Stripe, by storing payment options—have made a lot of headway in this respect.

Newer Web browsers like Arc are reimagining the interface to become more desktop-like, with applications and workspaces. If people start thinking of their Web browser as an application space, it could evolve consumers’ mental-model away from the operating system and back to the internet.

WASM provides a mature bytecode format for Web-based software/application delivery that’s more efficient and secure than Javascript, supporting a variety of languages from C++ to Rust.

A bit longer term: WebXR will eventually absorb more of the graphics performance boosts from WebGPU. Along with WASM, it may be possible to get native-feeling applications for spatial computing that runs in a browser.

WebGPU

More needs to be added about WebGPU and how significant it is. Spearheaded by Microsoft (and gaining a lot of support form Unity), this is truly a development that will change how graphics-intensive software is delivered over the Web.

In addition to delivering 3D graphics performance, it also means that AI inference can happen on a user’s device without dependence on centralized APIs. This is relevant for a range of use cases: TensorFlow already has a WebGPU backend, including support for models such as speech and gesture recognition, and Unity Sentis is creating a technology for bringing AI models into the runtime of your game.

Here are a few projects worth investigating if you want to look into what WebGPU can currently do, include both AI and graphics examples:

A developer (Madrigal) showing his homemade 3D engine and game using WebGPU

More on in-browser machine learning (ML) with WebGPU

Demo 3D environment using WebGPU. Won’t wow you relative to AAA graphics, but you can see how efficient the lighting on various surfaces is, and let’s you dream a bit about what people will make.

Next-Gen Rendering Pipelines

It’s amazing what a current 3D engine like Unreal 5 can do:

…but it’s also important to realize you won’t see this level of fidelity inside a commercial game right away. These scenes likely take many gigabytes and operate on top-of-the-line NVIDIA hardware. Still, it shows you what capabilities are on the horizon.

Unreal 5 technologies like Nanite and Lumen have gone a long-way to simplifying the workflow to build an environment like this: Nanite makes it possible to add high-polygon objects to a scene and let the engine optimize it for the scene; and Lumen spares developers from baking the lighting every time they want to adjust something. Software-based techniques are likely to continue to accelerate the ability for developers to go from imagination to the screen. However, these technologies won’t solve the problems of bandwidth, storage and memory that make a scene like the above possible—until more of this hardware makes it to the consumer.

On the other hand, there are emerging technologies that completely redefine the graphics rendering pipeline. One that’s gotten a lot of attention is Gaussian Splats, because they can generate high-fidelity scenes:

Gaussian Splats can deliver great-looking, highly-efficient imagery to the user—on par with the Unreal 5 example shown above. And with in-browser rendering via WebGPU, could eventually be another pillar of a Web-based future for gaming.

However, it’s important to recognize the current limitations of Gaussian Splats with respect to gaming:

Scenes generated with gaussian splats are not interactive. You can run around a beautiful scene, but you can’t change anything.

Developers need to sort out things like collision detection on their own.

Gaussian Splats are based on a point-cloud representation of the scene, rather than the geometry-based systems that are the entire current toolchain. This will require either new toolchains that manipulate point clouds directly, or perhaps hybrid approaches that combine geometry with Gaussian rendering techniques.

All of the above are already happening, but are mostly in the domain of SIGGRAPH presentations and research papers. Here’s a good, current GitHub resource of current research on Splats: awesome-3D-gaussian-splatting

What’s all this mean for game developers and the technology industry supporting them?

Short-term, the only games that could utilize Gaussian Splats would likely be games where navigating around a static scene is OK.

For real-time immersive games like RPGs and first-person shooters, the toolchain needs to be a lot more mature before this can be incorporated into shippable products.

Leveraging new rendering pipelines could be an opportunity for next-gen 3D engines (re-read the above section Cracks in the 3D Engine Market). This could become important for Unity and Unreal as well, if it means shipping higher-fidelity games to devices with lower specs than would be required in the Unreal 5 demo shown at the start of this section.

Strong PC Gaming on Steam

Relative to the gaming market overall, PC games have performed better than most categories. Steam shows where some of the current success is being found:

PC Gaming is a great place to develop: it’s where most people are enjoying Roblox and Fortnite; 2024 promises a great slate of products (I’m looking forward to Homeworld 3 and Hades 2!) This is one of the best markets to build for if you’re a team with a great idea. Why?

You can deliver the best graphics and gameplay performance that technology currently offers;

You have a variety of choices with where you want to deliver and monetize your game: everything from Steam, to supplying your own download links;

More of your revenue can be reinvested back into making great games and effective live ops—giving businesses greater sustainability;

You can build a robust modding community by providing editors and online communities, which leads to…

UGC Growing for PC Games

Creator-led platforms are not limited to Roblox, Minecraft and UEFN. Many individual games are also becoming hubs for paid creators as well. Overwolf is a platform for adding monetizable modding capabilities to PC games:

Here is the distribution of revenue to creators on Oversold:

Transmedia Inversion

Transmedia is the idea of narrative that spans multiple forms of media: particularizing video games and long-form video formats. In the past, most trans media originated on more traditional formats (television, movies, comic books) and then made its way to video games. I myself made several games like this: Game of Thrones Ascent, Star Trek Timelines, Walking Dead: March to War and Archer: Danger Phone.

But in 2023 we reached an inflection point: although making a “video game movie” isn’t exactly a new idea, they’ve always struggled to result in anything great. That changed in 2023 with examples like Last of Us, Dungeons & Dragons: Honor Among Thieves and the Super Mario Bros. Movie.3

This trend is extending into 2024, with the Fallout series is coming to Amazon Prime.

Unlike TV and movies, which linger for years and decades as static artifacts, games can and must evolve over the course of many years. Consequently, there are two aspects of transmedia game development that you’ve got to get right:

Having the right economic incentives in place to nurture a decade-or-longer partnership that benefits everyone

Having the right technology in place to support high content-creation velocity and agile live ops

Aligning the Incentives

The best way to deliver a transmedia game is to make sure that everyone has the right economic incentives so that they add-value to each other: by leveraging games as a means of promoting the traditional media, and incorporating new content into games (and vice versa) as quickly as you can, resulting in a “living world” experience for players. This is the way to create a re-engagement flywheel that benefits everyone.

In my experience, it’s hard to align incentives. People who license IP at most media companies are incentivized by short-term payoffs (their bonus check is often tied to the size of a prepay or guarantee) rather than long-term performance or the network effects that adhere to the original media. One way to solve this is through comprehensive ownership—everything from the traditional media to the games (WB is perhaps the best example of this). Otherwise, it takes an unusual level of trust, C-level buy-in, and carefully crafted incentives. In my experience, it’s challenging—but it is an enormous opportunity when the right business structure is in place.

The other pillar of success: building a transmedia game requires you to update content regularly (ideally, reflecting content in all media channels, with games and traditional media in sync), operate online events, and carefully tune experience to drive engagement and retention. Which brings me to…

Live Operations Must be More Efficient

Matt Ball pointed to this in his recent report:

Retention, not acquisition, is ultimately the real contest for a live services game – and the volume of content that is needed to sustain ongoing play is substantially higher than 5-6 years ago too. This isn’t just volume of cosmetics, but the underlying content players consume too, map updates, missions, weapons etc., and their velocity, too. It’s financially impractical for smaller-sized publishers and studios (e.g. 1047 Games) to have a large live services operation (people, plans, infrastructure) ready to go when their game launches - even though they naturally hope for a blockbuster open or at least second-base hit.

— Matt Ball, the Tremendous Yet Troubled State of Gaming in 2024

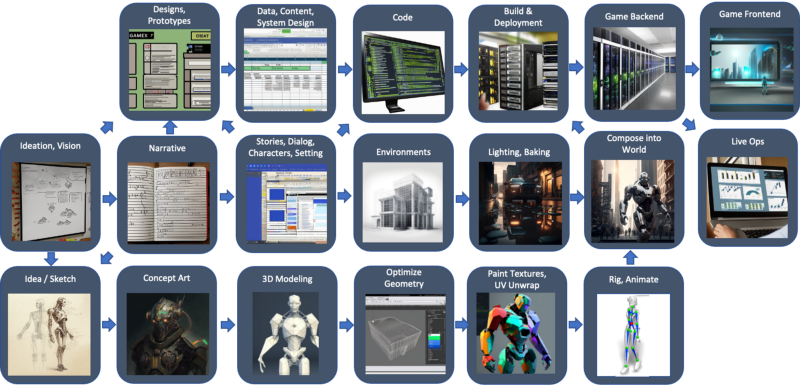

Game Development is Top-Down, which means that these technology decisions must be driven by the needs of the customer and organized around the team that’s most directly involved in content creation—not building technical components. It is about crafting living-world experiences with multiple media touchpoints, accelerating the velocity, operating cash-efficiently, personalizing player experience, iterating a game based on your players’ behavioral signals, and managing the funnel from top-to-bottom from user acquisition down to monetization and reengagement.

The problem is that live operations is technologically fragmented, few teams have all of the integration skills that are necessary, and it ought to be a content and business function more than an engineering job at most studios. Solving for this fragmentation by providing a more integrated, holistic approach to backend and live services is the opportunity my team has taken on at Beamable.

Generative AI

Generative AI is already having a significant impact on the production of games, starting with the illustration and concept art processes in games. As early as a year ago, the offshore art houses that many studios hire for asset creation started laying off people. Palworld also may4 have used generative AI as part of their workflow, which may be how a 10-20 person team created a $200M+ hit.

I discussed the Five Levels of Generative AI for Games last year, introducing a 5-level scale similar to what is used to assess advancement in autonomous vehicles:

Right now, 2D art creation is capable of high-levels of control: technologies like LoRA (Low-Rank Adaptation) simplify fine-tuning of diffusion models, which makes it easier to establish aesthetic consistency—and ControlNet pioneered the ability to exercise a high degree of control over posing of characters.

3D has a long way to go, but it’s improving. It is important to realize that when we’re talking about 3D, it’s a far more complex problem on multiple axes: not only generating models from 2D concepts (or from text prompts), but optimizing them; rigging them; animating them; composing them into scenes. All of this complexity means that 3D will likely take longer to mature than 2D did, but there’s a high likelihood that it will improve because of the large number of academic, corporate (especially NVIDIA) and startup teams working on the many problems

Initially, this work will be about accelerating parts of the 3D pipeline; later, it will be about integrating the overall workflow into a holistic process. As these technologies mature, I’d expect that studios will adopt it as rapidly as the 2D art is already making headway.

{kind=link}

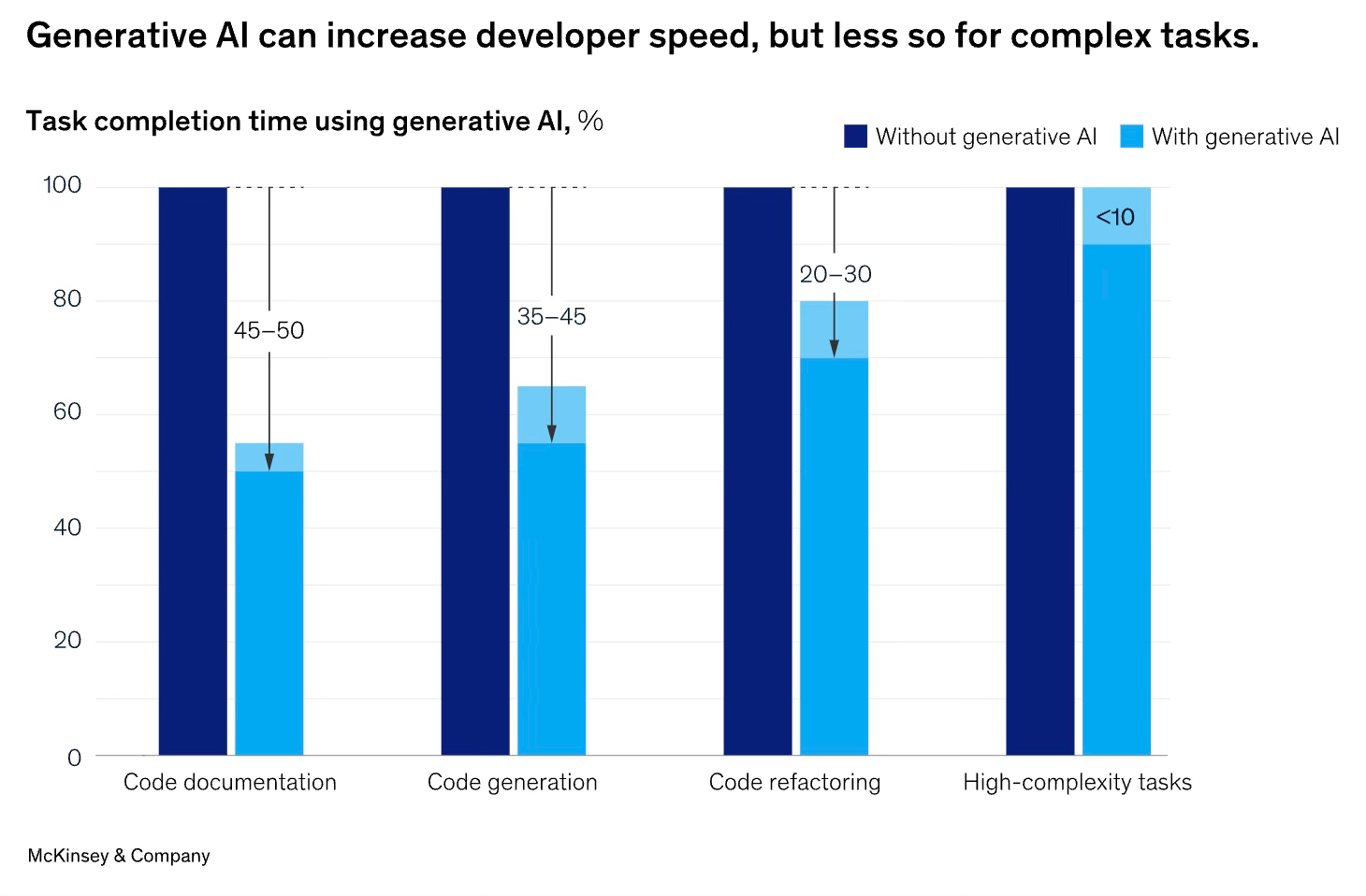

Of course, generative AI in games is not limited to production of art assets. It includes the use of technologies like CoPilot and ChatGPT to accelerate software engineering, with some work accelerated by a factor of 2x:

Likewise, generative AI is likely to impact audio, music and narrative development. Most of these asset types aren’t quite past the uncanny valley yet, but they’re getting close. And while social critics will bring up worries about a “content orouborus” (naturally, differentiated products will continue to stand out), consumer backlash (most likely a vocal minority who don’t represent the mass-market), labor dislocation, expectations of regulatory oversight, legal challenges or other philosophical concerns—developers who apply these technologies to build highly profitable business while delivering fun experiences want will reap the benefits.

Procedural + Generative AI

Procedurally-generated terrains and environments are already quite powerful: Gaia from Procedural Worlds is probably the most popular of these; Jason Booth, who I worked with on Star Trek Timelines and other games, has also made a line of tools for Unity (Megasplat, MicroVerse, etc.) which automate worldbuilding. At the level of 3D models, Sloyd.ai generates meshes by linking a text-prompt front-end to a parametric modeling system.

You’ll see these procedural systems continue to get more and more powerful, while adding LLM-based frontends to simplify interactions and iterations with the underlying systems.

In-Game Generative AI

The other aspect of generative AI is using these technologies interactively, delivering new game experiences that couldn’t have been possible before. Last year, my team won a hackathon, creating a D&D-style game that generates stories and skybox environments on-the-fly:

Eventually, you’ll be able to speak entire worlds into existence with generative AI. That’s the vision of the “Holodeck.” The CEO of Midjourney thinks we could see a version of this in 2024. My suspicion is that the first versions we see in 2024 will be enhanced variants of the tech demo we created above, and there will need to be far more progress on 3D before this can happen. I also expect that the most compelling versions will—at first—be a hybrid of generative and procedural techniques.

There are likely to be plenty of other games that play with game designs incorporating generative AI. Most of the examples this year are likely to be experimental and a bit rough; but there’s always the chance of a breakout hit with a unique idea—this is the game industry after all, and you never quite know what will work.

But there is one thing we can say with relatively certainty: cloud-based generative AI costs money. This cost will be an operating cost for any game that uses it. Even with the best free-to-play economies, these costs are likely to be a challenge for many developers. For that reason, deploying AI models on-device (where the end-user shoulders the energy bill) are likely to be far more scalable for many types of games. Outside of games, the Rabbit R1 demonstrates how embedded AI may become disruptive to cloud-based inference.

Open Economy Games

Magic the Gathering and Pokemon are examples of “open economy games” where players own the physical gaming assets (cards) and can trade them with whoever they want. The gameplay systems are then organized around the fact that this type of freeform exchange will happen between players.

To a lesser degree, open-economy games have also existed in some online versions of Magic the Gathering (although you trade through their platform, rather than directly with other players). The largest online game with a player-to-player trading economy is probably the market for Counterstrike Skins. Roblox also features a trading system for avatar personalization, which can often work across a range of different Roblox games.

Magic the Gathering, Counterstrike Skins and Roblox avatars are an existence-proof for the desirability of trading systems for online game assets. To move beyond specific walled-gardens, we’ll need an interoperable technology that allows value exchanges to happen without intermediaries. Although blockchain has been plagued by bad games, bad actors and outright thieves—it remains the technology most likely to enable open-economy games.

Open-economy games can also be about more than the exchange of assets; it can be about the composition of content and code in a way that builds upon each other, enabling players to create their own tournaments, worlds and “house rules.”

But what’s needed most of all for blockchain games to flourish is a handful of games that are good. As I began this article with, we need people saying, “This game is fun.” Until then, it won’t matter. There are a few games on the horizon which I’m excited about: Mystery Society, Wildcard Alliance, and Shrapnel—to name a few.

Beside the composability and interoperability potential of blockchain, it may also be the technology that could address the Hard Problem of Provenance with generative AI: identifying where and who a particular generative asset was derived from, which has applicability to everything from copyright concerns to understanding the sources of knowledge.

Takeaways

Here are a few themes that emerged as I assembled some of the opportunities and trends I’ve observed:

Games need to be great to succeed, and “great” means connecting with and understanding specific audiences

Don’t get caught up in either hype, or anti-hype

Lean, agile teams have an unfair advantage—and can create enormous hits with outsized returns

IP will continue to be important—and games will lead the way

Technologies need to deliver great experiences for the mass-market while being easy for developers to adapt to their workflow

Developers are hungry for platforms that can deliver great experiences while enabling them to control their destiny

2024 is about efficiency, focus, and quality

Further Reading

Game Development is Top-Down discusses how developers produce the most value when focused on design and experiential iteration.

The Direct From Imagination Era Has Begun is where we’re eventually heading.

Five Levels of Generative AI for Games is a way to think about progression of generative AI in game development.

My company Beamable is building the holistic infrastructure for everything that happens in the cloud, from live ops to backend servers. If that’s relevant for your game (and shouldn’t it be?) we’d love to help!

Much of the internal debates in the game industry can be summed as manifestations of Hume’s is-ought problem.

I’m definitely one of the consumers who loves Apple products. I’m writing this on an M2 MacBook Pro. I’m wearing an Apple Watch Ultra. I use an iPhone 15 as my daily phone. I preordered a Vision Pro. I love so much of what they’re doing with their products, from the semiconductors all the way up to the UI innovations in the operating system. Anything written here is written with love and a hope that we might return to a more developer-friendly ecosystem that helped Apple make it what it is today.

It’s also worth noting that games about making video games are becoming more popular, like the Tetris movie, or the the Mythic Quest series (both on Apple TV).

Reports on generative AI in Palworld are unconfirmed, although the CEO has mentioned the use of genAI in previous projects.

Such a great and thorough piece. Thank you for the insights.

A lot of people lately had been talking about a crash of sorts. Do you think they're on to something? Or are they just blowing smoke?